Chad Anderson is the founder and CEO of Area Capital, the place he has been pioneering funding within the area economic system for over a decade. He’s additionally the writer of “The Area Financial system,” printed by Wiley. Disclosure: Anderson is an early investor in SpaceX, together with dozens of different area corporations.

Each quarter, Area Capital tracks each greenback flowing into the area economic system. The midyear numbers are in: Non-public funding totaled $31.6 billion throughout 129 area corporations within the first half of 2026 — greater than all of 2025, making this the strongest 12 months on file for the area economic system, with two quarters nonetheless to go.

Since SpaceX (SPCX) got here on-line in 2009, the area economic system has attracted $488 billion throughout greater than 2,400 corporations. If the SpaceX preliminary public providing (IPO) felt like a climax for the sector, the info suggests it was simply the opening act.

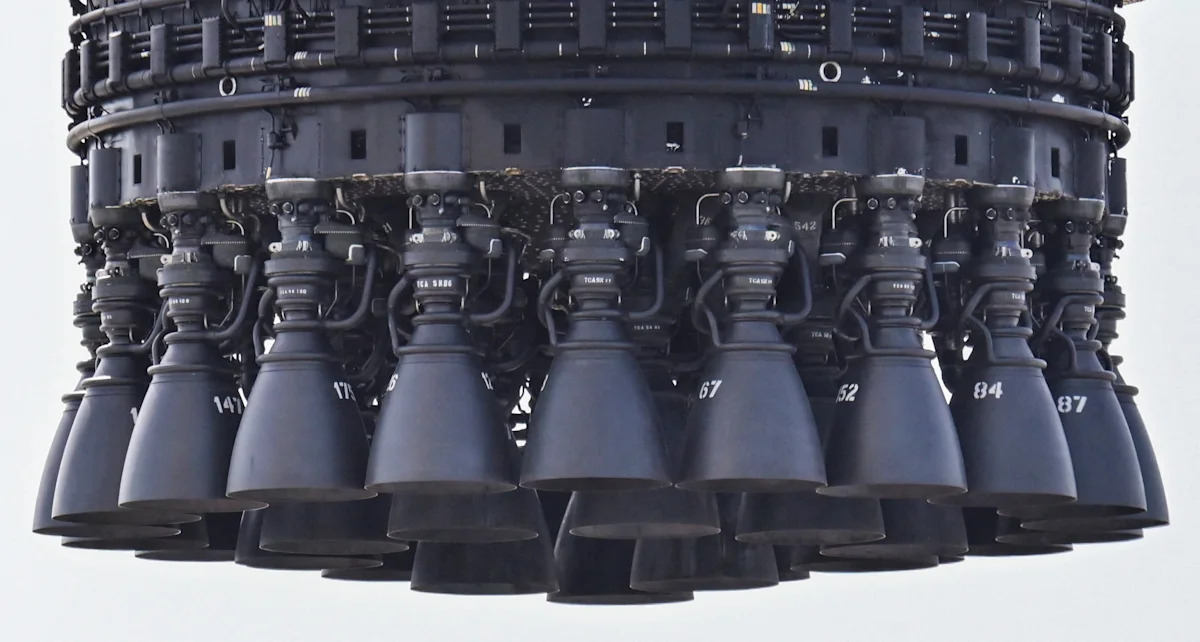

Thirty-three Raptor engines grasp from the underside of Booster 20 at Pad 2 because it prepares to roll again to SpaceX’s launch manufacturing facility in Starbase, Texas, U.S., July 17, 2026. REUTERS/Steve Nesius ·REUTERS / REUTERS

No occasion looms bigger over these numbers than that IPO. The market lastly has a public benchmark for the corporate that has carried out greater than some other to form the fashionable area economic system. But virtually instantly, the dialog shifted from valuation to id, with some analysts asking whether or not SpaceX ought to even be thought-about an area firm anymore.

That query misses the purpose. Wall Road has all the time categorized area below aerospace and protection — {hardware} companies valued on authorities contracts and program backlogs. That field now not matches. The worth in area is accruing in layers that analysts cowl elsewhere: communications, compute, and AI.

SpaceX has made the misclassification not possible to disregard.

The primary AI IPO

SpaceX’s S-1 submitting didn’t describe a rocket firm. It described “the one firm constructing the built-in {hardware} and software program infrastructure of the long run throughout area, connectivity, and AI.”

Take a look at the sequence of strikes. SpaceX merged with xAI earlier than the IPO. Days after going public, it acquired Cursor in a $60 billion all-stock deal. In the identical quarter, it signed AI compute agreements with Anthropic (ANTH.PVT) and Google (GOOG, GOOGL) value roughly $26 billion in annualized income, greater than doubling the income it took the corporate twenty years to construct. It is going to make AI chips with Terafab for orbital knowledge facilities.

There is a historic sample right here. Commonplace Oil owned the wells, refineries, pipelines, and tank vehicles. Carnegie Metal owned the mines, mills, and railroads. SpaceX is making an attempt one thing comparable for the AI period by integrating launch, satellites, orbital compute, and AI right into a single platform.

Area is turning into AI infrastructure, and AI is turning into the financial engine of area. Simply as each firm of immediately is a expertise firm, each firm of tomorrow might be an area firm. SpaceX is solely the primary to be priced that manner.

The exit argument is over

SpaceX’s long-term affect extends nicely past its $1 trillion-plus valuation. For a decade, the knock towards the area economic system was its lack of exits. That argument was refuted in Q2.

The SpaceX IPO is the most important liquidity occasion in enterprise capital’s historical past. It surpassed the full-year exit worth of 2021 and generated extra exit worth than each VC-backed IPO of the previous decade mixed. It returned roughly 171 instances the capital the corporate raised. Uber (UBER), at its 2019 debut, returned 2.7 instances. That is the distinction between proudly owning the functions and proudly owning the infrastructure they’re constructed on.

The Q2 Area IQ report counted $90.3 billion throughout 42 exits within the quarter, together with 35 acquisitions and 7 public debuts. Jeff Bezos’s Blue Origin acknowledged for the primary time that it’ll want outdoors capital to scale and did not rule out going public. The IPO window that was shut for years is now open, and area corporations are strolling via it.

SpaceX creates each alternative and stress

SpaceX’s relentless discount in launch prices created immediately’s industrial area economic system, and almost each profitable area enterprise rides that tailwind. However the market is adjusting to a special actuality: SpaceX is reportedly pulling again on rideshare to prioritize its personal Starlink and AI satellites, alarming small satellite tv for pc operators that depend on that capability.

Eclipse Area founder Derek Huerta, a part of the core group that constructed and scaled Starlink, calls this a reversion, not a collapse. The previous 5 years of low cost, frequent rideshare have been the anomaly. Falcon 9 was constructed to serve Starlink, and everybody else rode the surplus capability.

That reversion is the place the chance lies. A decade in the past, small launch corporations constructed capability forward of demand, and it killed a number of of them. Immediately, demand is operating forward of provide, with new automobiles coming on-line towards dedicated order books. As capability tightens, entry to orbit itself turns into extra precious, creating alternatives past rocket makers — within the corporations that dealer, handle, and allow launch providers.

The following decade is already taking form

Deal exercise broadened at the same time as capital concentrated behind perceived class leaders. Prometheus raised a $12 billion Collection B, the most important deep tech spherical ever for bodily industrial engineering, to construct AI that designs, manufactures, and operates bodily property. There are actually 106 non-public area economic system corporations value greater than $1 billion, with a mixed valuation of roughly $648 billion.

Most of that worth stays locked in non-public markets, however the path to public publicity is widening. Along with SpaceX, HawkEye 360 (HAWK) listed this quarter. Rocket Lab (RKLB) is vertically integrating in public view. A slate of late-stage candidates is lining up behind them — watch Blue Origin’s capital plans, the Iridium deal’s anticipated 2027 shut, and the subsequent wave of IPO filings.

{kind=link}