Lower than a decade in the past, Southeast Asia was overwhelmingly a money society. Road distributors, taxi drivers, eating places, and even some lodges dealt solely in paper payments and cash. In case you visited Bangkok or Ho Chi Minh Metropolis in 2015, you carried money for nearly every thing.

In the present day, that world is barely recognizable. QR code funds have swept throughout the area at a tempo that caught even essentially the most optimistic fintech observers off guard. In Thailand, Vietnam, the Philippines, Indonesia, and past, scanning a code along with your cellphone has grow to be the default option to pay.

In Canada and the West, in the meantime, bank cards stay king. We faucet our playing cards at espresso retailers, grocery shops, and fuel stations, racking up Aeroplan factors and MR factors alongside the best way. Your entire Miles & Factors ecosystem is constructed on the belief {that a} Visa or Mastercard works in every single place.

That assumption breaks down the second you land in Southeast Asia. Understanding how fee tradition diverged between East and West, and realizing learn how to bridge the hole, can save Canadian travellers from attempting to find ATMs, carrying wads of money, and overpaying at airport forex desks.

How Asia Leapfrogged Credit score Playing cards

The numbers inform a hanging story. In accordance with a 2022 survey, practically 60% of Southeast Asian respondents already used QR funds. In China, the saturation is much more excessive, with roughly 90% of city shoppers and 90% of outlets utilizing QR funds each day.

By 2024, cell fee transaction values surpassed card-based transaction values in each single Southeast Asian nation. By 2028, non-digital funds are projected to account for simply 6% of whole e-commerce transactions within the area.

How did this occur? Asia largely skipped the bank card period solely.

In Canada, bank cards proliferated as a result of we had well-established banking infrastructure, excessive charges of checking account possession, and retail networks that invested closely in card terminals. The rewards ecosystem grew on prime of that basis.

A lot of Southeast Asia was basically completely different. Massive parts of the inhabitants have been unbanked or underbanked. Card terminals have been costly for small retailers. The infrastructure merely wasn’t there.

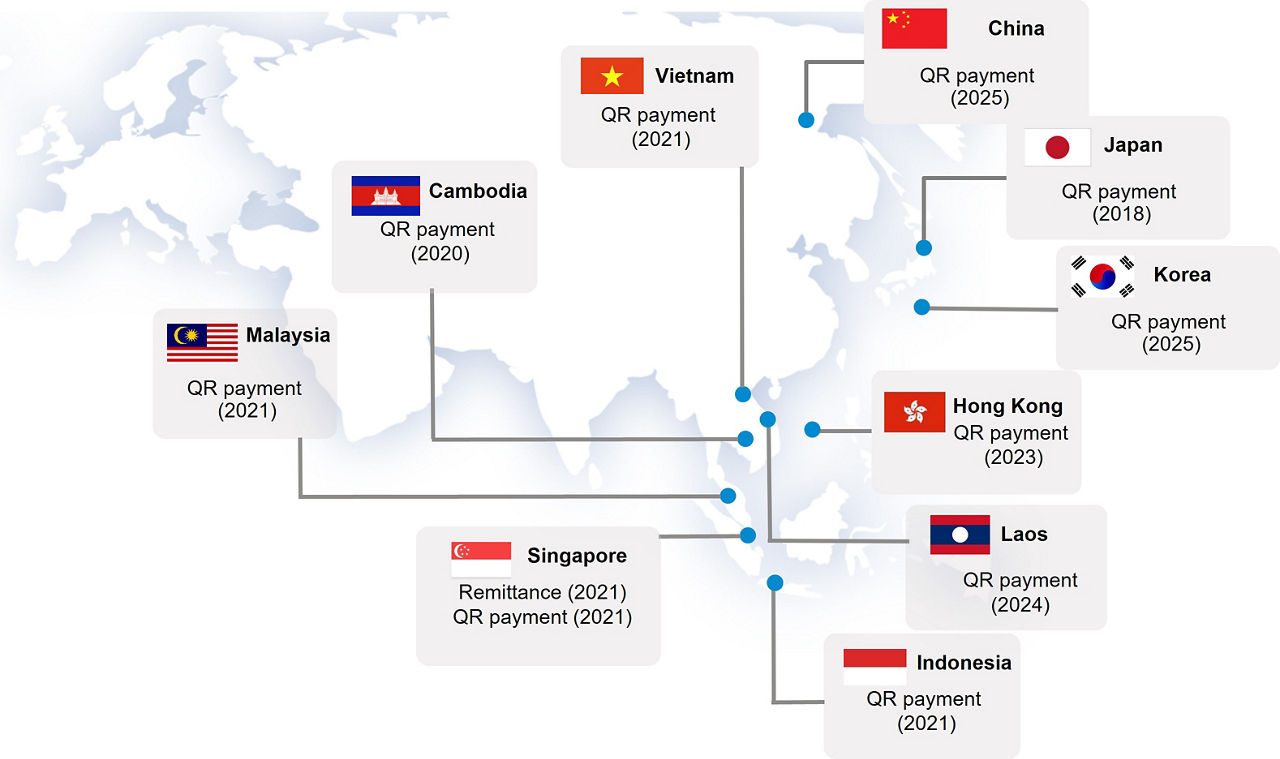

When smartphones grew to become ubiquitous, these markets leapfrogged immediately from money to cell funds. QR codes have been low-cost to implement. A service provider simply wants a printed piece of paper. Governments actively promoted interoperable methods. Thailand constructed PromptPay. Indonesia created QRIS. Vietnam developed VietQR. The Philippines launched QR Ph. Malaysia rolled out DuitNow QR.

The result’s an ecosystem the place the road meals vendor, the tuk-tuk driver, and the evening market stall all settle for QR funds, however many will not settle for your Visa or Mastercard.

How QR Funds Truly Work Beneath the Hood

From the surface, QR funds look easy. Scan a code, cash strikes. Beneath the hood, the infrastructure varies considerably by nation, and a few of it’s extra technologically superior than you would possibly anticipate.

The normal rails

Most nationwide QR methods in Southeast Asia run on standard real-time fee infrastructure. Thailand’s PromptPay, as an illustration, is constructed on change expertise developed by Vocalink (a Mastercard firm) and settles via BAHTNET, the Financial institution of Thailand’s real-time gross settlement system. It processes over 75 million transactions each day, all flowing via ISO 20022 messaging requirements and open APIs connecting the nation’s banks in actual time.

Indonesia’s QRIS operates equally, connecting 40 million retailers and 57 million customers via BI-FAST, Financial institution Indonesia’s prompt fee clearing system. Vietnam’s VietQR, launched in 2021 by the Nationwide Fee Company of Vietnam, grew 62% in transaction quantity and 151% in worth year-over-year in 2025.

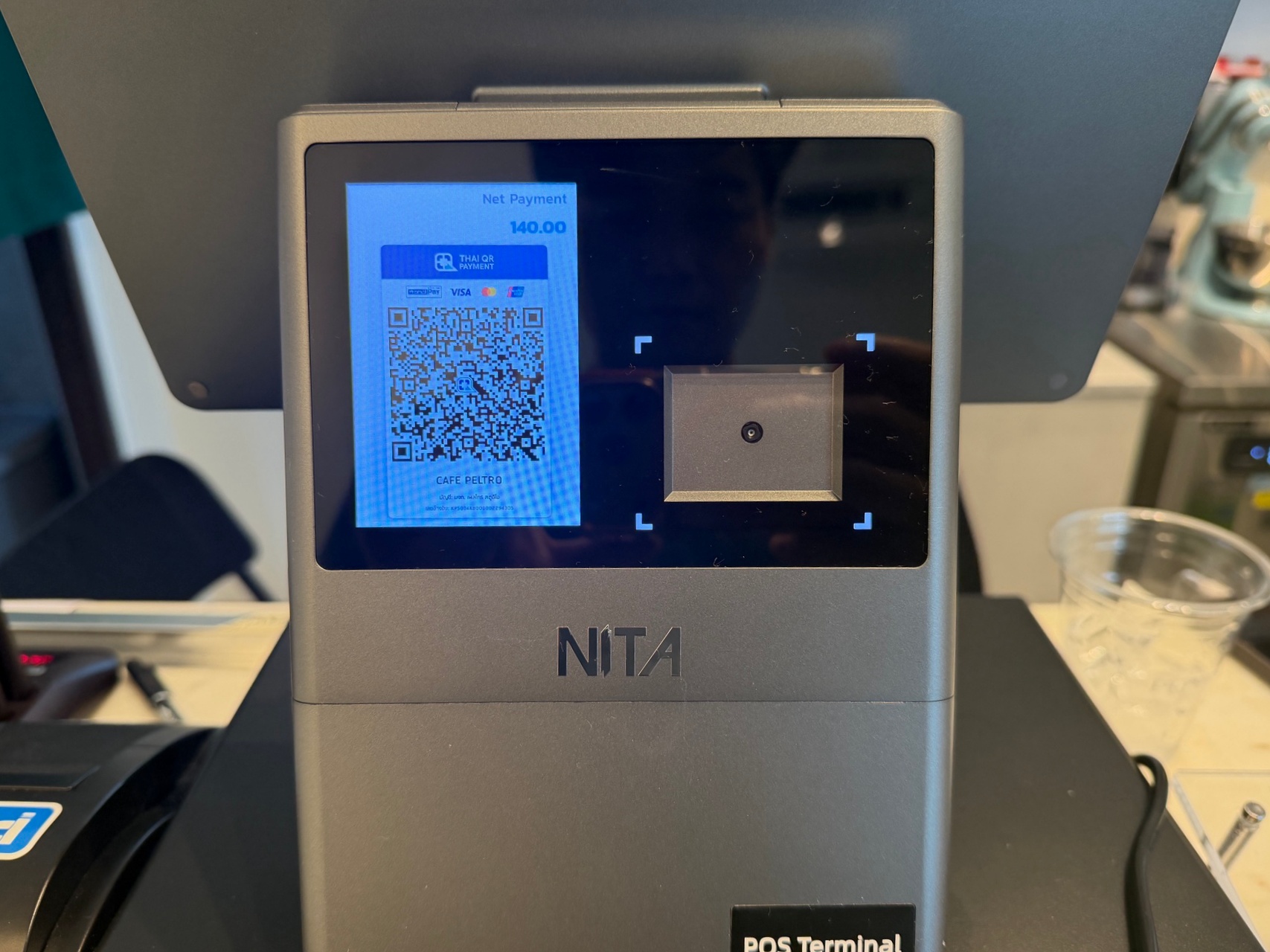

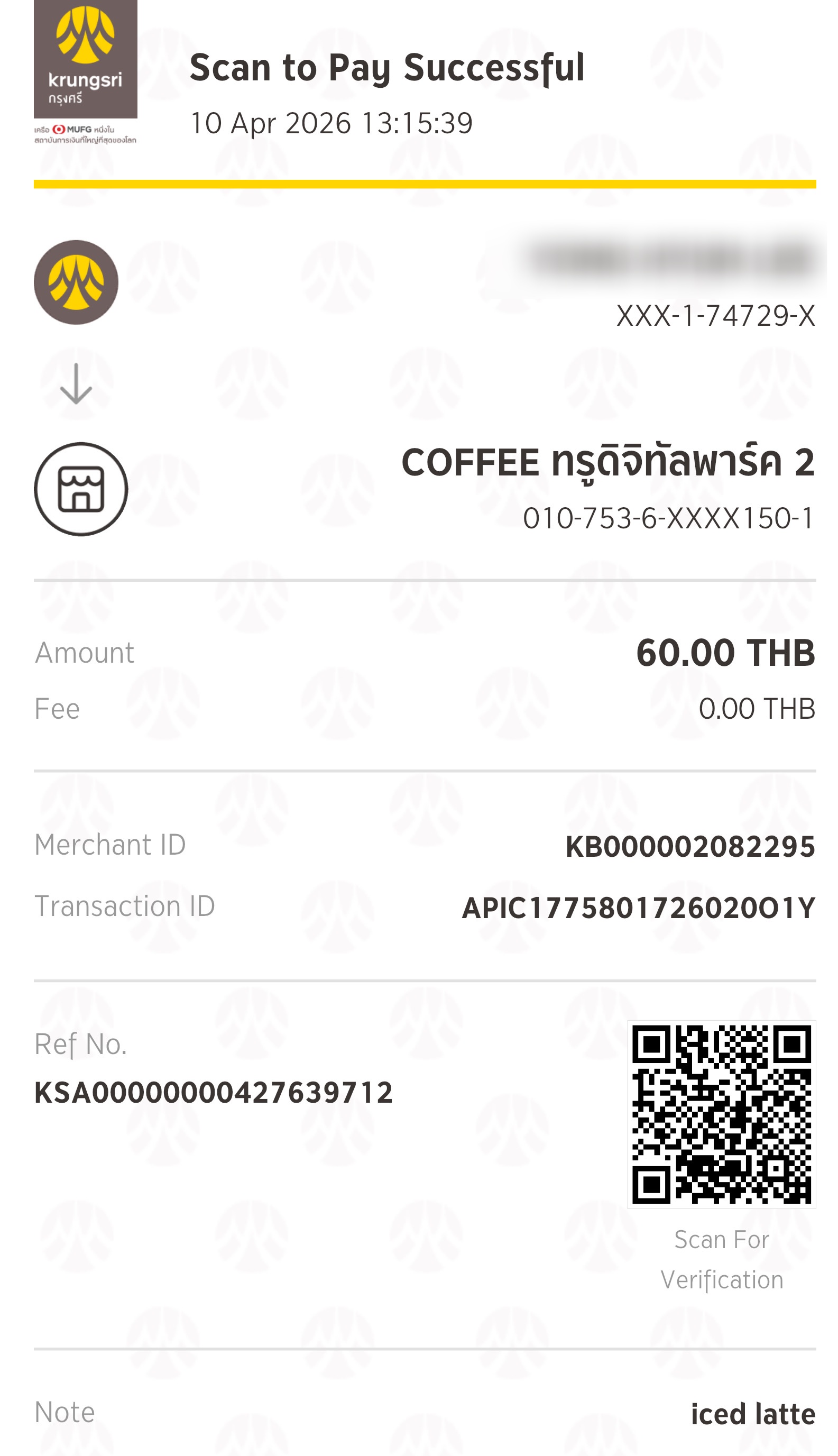

These methods work via two sorts of QR codes. Static codes are the laminated ones you see taped to a vendor’s stall, staying the identical for each transaction and requiring you to enter the fee quantity manually.

Dynamic codes are generated per transaction by a POS system, with the quantity already pre-filled. You simply affirm and pay.

The place blockchain enters the image

The newer layer is blockchain-based settlement, notably for cross-border funds. Ant Group (Alipay’s father or mother firm) launched one of many world’s first blockchain-based cross-border remittance companies again in 2018, utilizing distributed ledger expertise to allow real-time Hong Kong–to–Philippines transfers via AlipayHK and GCash.

In Southeast Asia, this integration is accelerating. Vietnam’s VietQR now incorporates blockchain expertise and stablecoin adoption. Thailand’s PromptPay infrastructure can facilitate stablecoin funds each domestically and internationally. Singapore-based StraitsX is constructing a regulated stablecoin ecosystem that mixes fiat stability with blockchain effectivity for cross-border QR funds.

The attraction of blockchain on this context is not cryptocurrency hypothesis. It is the settlement layer. Conventional cross-border funds route via correspondent banks, incurring delays and costs at every hop. Blockchain-based settlement can cut back that to near-instant, with a clear ledger that each events can confirm.

For the typical vacationer scanning a QR code at a Bangkok noodle stall, this backend complexity is invisible. Your fee goes via in seconds no matter which rails deal with it. The place it issues extra is within the cross-border interoperability layer, which is why a Malaysian vacationer can use DuitNow to pay at a Thai service provider, and why UnionPay is now linked with fee methods throughout Cambodia, Indonesia, Vietnam, and Malaysia.

The Canadian Traveller’s Dilemma

In case you’ve travelled to Bangkok, Ho Chi Minh Metropolis, or Manila not too long ago, you have possible skilled this firsthand. The upscale resort accepts your bank card. The airport retailers settle for it. The chain eating places settle for it.

Every little thing else? Money solely, or QR.

This creates an ungainly state of affairs for Canadian travellers who’ve constructed their whole journey technique round bank card earn charges. You possibly can’t earn 3x factors on eating if the restaurant would not settle for your card. You possibly can’t acquire Aeroplan factors at a road meals stall that solely has a QR code taped to the counter.

Even the retailers that do settle for bank cards typically tack on their very own guidelines. Minimal buy quantities are widespread, and a few retailers add a surcharge on prime of the invoice to cowl the processing price.

The normal fallback is money. Hit an ATM, carry a wad of baht or dong, and hope you aren’t getting shortchanged.

The price math on money has really improved not too long ago. The Wealthsimple Pay as you go Mastercard now reimburses international ATM charges, which arguably makes ATM withdrawals the lowest-fee option to get native forex. You are successfully simply paying the Mastercard community unfold.

Personally, although, I nonetheless hate carrying a pile of money and cash. So long as a QR possibility’s charges aren’t outrageous (say, above 5%), I am going to take the comfort and the clear digital path over a pocket stuffed with small payments.

Alipay and WeChat Pay opened restricted entry for worldwide guests in China, however the setup course of is cumbersome, typically requires a Chinese language cellphone quantity, and the performance stays restricted. In Southeast Asia, there’s been even much less infrastructure for foreigners to entry native QR fee rails.

That is beginning to change. A handful of fintech instruments now let Canadian travellers faucet into native QR networks with no native checking account.

Bridging the Hole: Sensible and Moreta Pay

Two instruments stand out for Canadian travellers who wish to pay through QR in Southeast Asia. One you most likely have already got. The opposite is purpose-built for this precise drawback.

Sensible

If you have already got a Sensible account (and in the event you’ve learn our information to one of the best methods to get international money for journey, you possible do), chances are you’ll not understand it will probably scan QR codes too. Sensible has quietly rolled out QR fee assist throughout a number of networks.

The protection consists of Alipay+ (a cross-border service provider community operated by Ant Group, distinct from China’s home Alipay app) which works at collaborating retailers throughout Thailand, Malaysia, and Singapore, QR Ph within the Philippines (accessible to all Sensible clients), and PayNow in Singapore (restricted to enterprise funds for non-residents, with a 1,000 SGD per-transaction cap). Swiss QR-Invoice and Hungary’s Qvik spherical out the checklist for European locations.

The attraction right here is simplicity. You have already got the app, you have already got balances loaded, and Sensible’s mid-market alternate charges are among the many finest accessible to Canadians. In case you’re heading to Thailand, the Philippines, or Singapore, verify whether or not your Sensible app’s QR scanner covers what you want earlier than downloading anything.

The limitation is protection. Sensible would not assist Vietnam’s VietQR, Indonesia’s QRIS, or Cambodia’s KHQR. It can also’t scan WeChat Pay or Alipay QR codes in mainland China immediately, although you’ll be able to add your Sensible card to these apps individually. For nations outdoors Sensible’s QR community, you will want an alternative choice.

Moreta Pay

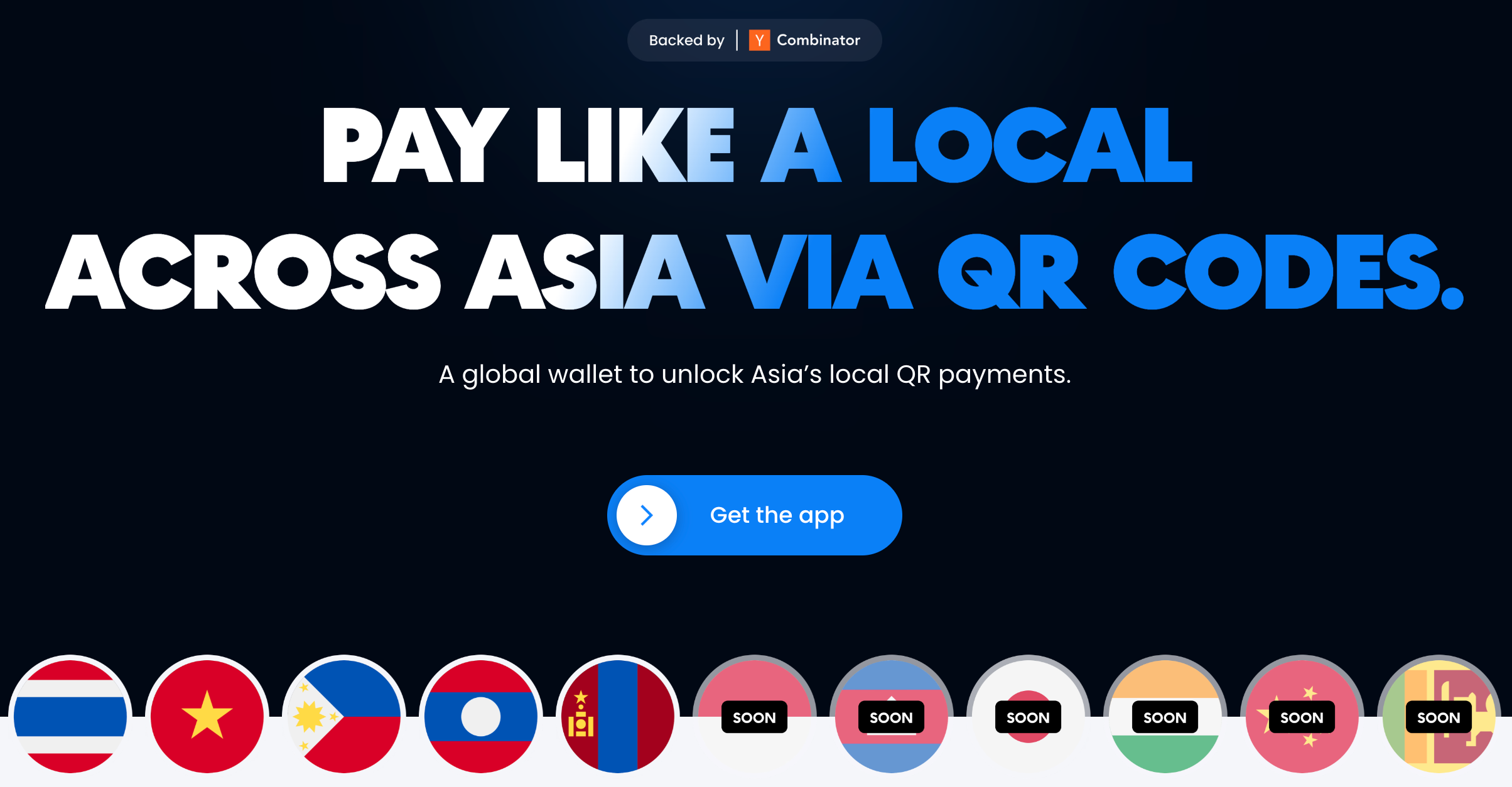

Moreta Pay is a Y Combinator–backed fintech constructed particularly for this hole. The place Sensible added QR as a function on prime of its multi-currency platform, Moreta was designed from scratch to let worldwide travellers scan and pay with the identical QR codes locals use.

The app integrates immediately with native fee networks. PromptPay and ThaiQR in Thailand, plus equal methods in Vietnam, the Philippines, Cambodia, Laos, Mongolia, and Indonesia. Once you scan a product owner’s QR code with Moreta, your fee goes via the identical rails an area would use. The service provider sees a traditional home fee. You see the price in your house forex with the alternate charge displayed earlier than you affirm.

On pricing, Moreta makes use of a 0.6% unfold on the mid-market alternate charge with no further markup. In Thailand particularly, there is not any transaction price in any respect. In different supported nations, a 1.5% transaction price applies per fee.

For Canadian travellers, there is a nuance to funding your Moreta pockets. Canadian-issued credit score and debit playing cards aren’t immediately supported for card top-ups on the time of writing. Nonetheless, you’ll be able to fund through Apple Pay or Google Pay utilizing your Canadian playing cards, which routes the transaction via Apple or Google’s fee community reasonably than processing the cardboard immediately.

The economics rely on the quantity you are loading. For smaller top-ups, Apple Pay is extra handy with minimal price overhead. For bigger quantities, linking a USD checking account (which you’ll be able to arrange via Sensible) avoids card-processing charges solely and provides you higher charges at scale.

Selecting between them

In case you’re visiting Thailand, the Philippines, or Singapore and have already got Sensible, begin there. It is one much less app to arrange, and also you’re already conversant in the way it works.

Moreta fills the gaps. Vietnam, Indonesia, Cambodia, Laos, and Mongolia are all lined by Moreta however not by Sensible’s QR scanner. In case your itinerary spans a number of Southeast Asian nations, Moreta’s broader native community protection makes it the extra versatile possibility.

Both manner, evaluate the entire value (alternate charge unfold plus any transaction charges) to the standard 2.5% international transaction price on most Canadian bank cards, and each come out forward. Particularly when the choice is not any card acceptance in any respect.

An Sincere Tackle the Person Expertise

I will be direct about this. QR funds are higher than carrying a pile of money and cash. However they’re nonetheless not as handy as tapping a cell pockets or a contactless card.

The method entails extra steps than you are used to. It’s worthwhile to hearth up the app, level your digital camera on the QR code, and look forward to it to scan. With static QR codes (the type you will discover at most smaller retailers), you then must key within the buy quantity your self. This introduces the opportunity of human error, whether or not that is mistyping a digit or getting confused by unfamiliar forex denominations with a lot of zeros.

After getting into the quantity, you affirm the transaction, then present the fee affirmation display screen to the workers. It is 4 or 5 distinct steps versus the only faucet of a contactless card. At a busy meals court docket or while you’re juggling baggage and a plate of pad thai, that distinction is noticeable.

There’s one upside that playing cards do not supply, although. Each QR transaction generates a publicly viewable fee slip. A clear report that each you and the service provider can entry.

In case you ever must dispute a cost or monitor down a refund, this eliminates the back-and-forth that may plague bank card chargebacks. With a card dispute, you are typically caught in a triangle between your financial institution and the service provider, every claiming the opposite hasn’t processed the refund. With a QR fee slip, you’ll be able to merely ask the service provider to drag up the transaction report. It is proper there, timestamped, with the quantity and standing seen to each events. No ambiguity, no ready weeks for a chargeback investigation. Simply “present me the slip.”

What This Means for Your Factors Technique

None of this implies your bank card technique is out of date. Inns, airways, tour operators, and main retailers all through Asia nonetheless settle for playing cards. You may nonetheless earn factors on the big-ticket gadgets. No international transaction price playing cards stay important for these purchases the place plastic is accepted.

What’s altering is the lengthy tail of spending. The meals, the transport, the small purchases that collectively make up a good portion of your journey finances. In nations the place QR dominates, that spending merely is not accessible to your bank card anymore, irrespective of how premium it’s.

Canadian travellers heading to Southeast Asia ought to consider their fee technique in two tiers. Tier one is your journey bank cards for lodges, flights, and bigger retailers. Tier two is a QR fee answer (or money) for every thing else.

In case you monitor each greenback of spend for factors optimization, this can be a shift value acknowledging. The road meals finances in Thailand could be $30–50 (CAD) per day. Over a two-week journey, that is $400–700 in spending that will not contact your bank card earn charges it doesn’t matter what you do.

The Larger Image

The QR fee shift in Asia is not slowing down. Cross-border interoperability is increasing quickly. UnionPay is now linked with fee methods in Vietnam, Indonesia, Malaysia, and Cambodia, creating seamless regional fee networks that do not contain Visa or Mastercard in any respect.

For Canadian travellers, the hole between “how I pay at residence” and “how I pay overseas” is widening in components of Asia, even because it narrows in Europe and the Americas the place contactless playing cards stay dominant.

Instruments like Sensible and Moreta Pay characterize the primary wave of bridges throughout this divide. Sensible is already a well-recognized a part of many Canadian travellers’ toolkits, and its increasing QR assist makes it a simple entry level. Moreta goes deeper into native networks that Sensible hasn’t reached but. Each are nonetheless evolving. As extra Canadians journey to Southeast Asia, anticipate the protection and competitors to enhance.

Conclusion

If I am heading to Thailand or Vietnam in 2026, here is what I would really do. Test whether or not Sensible’s QR scanner covers my locations first, since I have already got the app loaded and funded. For nations Sensible would not attain, arrange Moreta Pay earlier than departure and fund it through Apple Pay. Bank cards keep in rotation for lodges, flights, and wherever plastic is accepted.

For every thing at road degree, I would settle for that not each baht I spend goes to earn rewards. A 0.6% alternate unfold via Moreta or Sensible’s mid-market charge beats the 5% markup at an airport forex desk. It beats the ATM withdrawal price plus no matter charge your financial institution decides to provide you. And it beats fumbling with unfamiliar payments whereas a line types behind you on the pad thai stall.

Bank cards aren’t going away. They’re simply not common anymore. The earlier we adapt to a two-system world, the much less friction we’ll encounter on the bottom.

{kind=link}