Denis Ladegaillerie has had time to assume.

Within the months it took to orchestrate the complicated equipment required to take Imagine non-public – through a joint consortium with TCV and EQT – the CEO has been observing. Analyzing. Drawing conclusions not nearly his personal $2 billion firm, however in regards to the basic dynamics reshaping the worldwide music enterprise.

The outcome? A collection of knowledgeable takes that problem typical knowledge at each flip.

On market construction: With 70% of document trade revenues now coming from outdoors the Prime 200 in most markets, Imagine has constructed a complete enterprise philosophy round what Ladegaillerie calls “middle-first” considering – basically totally different instruments, offers, and methods than these designed for famous person economics.

On the Common/Downtown merger that’s at present exercising regulators and a few indie rivals? Ladegaillerie is relaxed.

“Do I believe that’s going to alter something for us? I can’t communicate for the trade, however as an organization, we really feel superb about our capacity to compete,” he says flatly.

The European Fee, he suggests, ought to maybe spend extra time pondering why algorithmic suggestions are creating an Anglo-American monoculture throughout non-charting streams in most EU markets.

“The primary challenge for EU/UK lawmakers might not be the Downtown merger,” says Ladegaillerie. “It’s 28% of streams being from native artists within the UK, 36% in Germany, 41% in France.”

On the expertise that basically issues: Neglect AI panic (“marginal income alternative, marginal risk”). Ladegaillerie is way extra targeted on Spotify‘s Discovery Mode, which he claims Imagine is utilizing “at a bigger scale than anybody else” – with 98% of tracks exhibiting optimistic monetary returns.

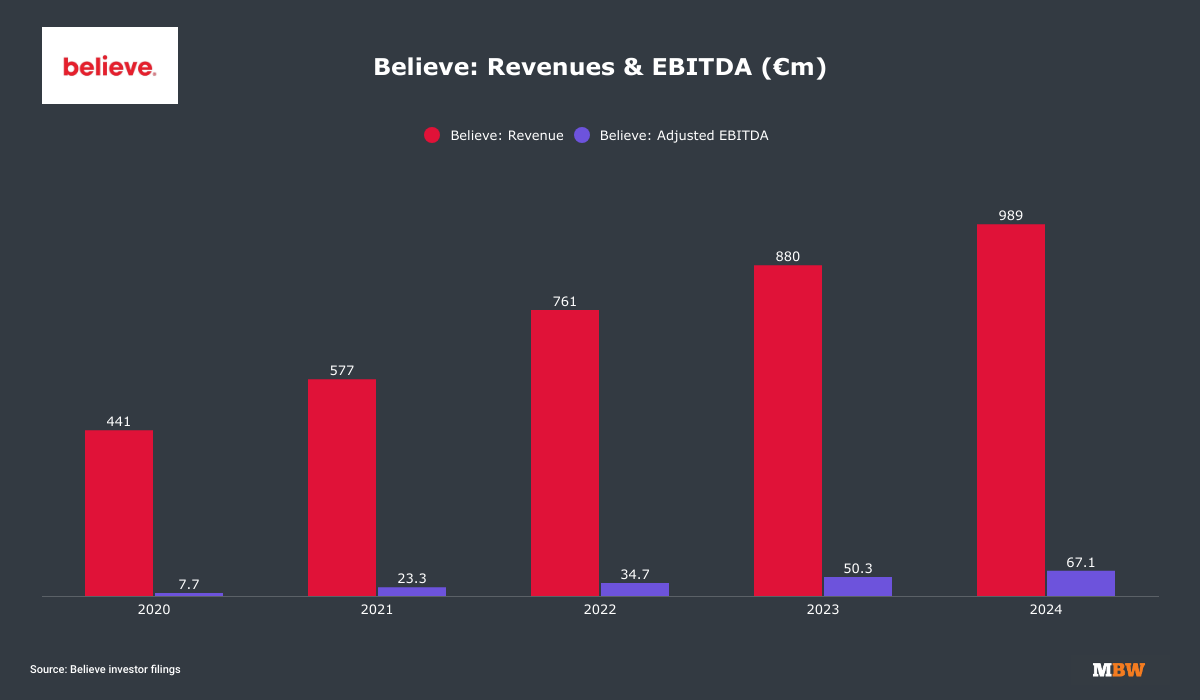

Once I meet up with Ladegaillerie in London, Imagine has simply accomplished its transition again to personal possession, valued at round USD $2 billion.

The corporate that began in 2005 as a digital distribution pioneer now operates throughout 50+ international locations, serving everybody from bed room producers through TuneCore to established impartial labels and artists looking for refined advertising companies.

The timing of our dialog is especially revealing.

Whereas bigger rivals are asserting substantial cost-cutting packages, Ladegaillerie says Imagine’s headcount is rising. Whereas others fear about streaming saturation in mature markets, he sees “loads of development” forward. And whereas segments of the enterprise obsess over consolidation and market focus, he’s quietly constructing a machine that thrives on the precise reverse rules.

“We’re in a brand new period of Imagine,” he says, outlining a 10-year strategic plan dubbed “From Entry to Success”.

“The previous decade has basically been about leveraging expertise to democratize market entry, which is what we’ve seen with increasingly more impartial artists capturing market share. However entry doesn’t imply success,” he says.

“The years forward will likely be outlined by how, on this new panorama, document labels drive their artists to success. That’s in regards to the high quality of the music, the manufacturing, the standard of [your] movies, and the way refined you could be round the entire digital viewers improvement levers.”

What emerges from our dialog isn’t simply Ladegaillerie’s pleasure over the way forward for the “center tier” or impartial distribution. It’s a complete worldview about the place worth lies in fashionable music — one which sees the trade’s present evolution not as a risk to be managed, however as a possibility to be seized…

What are the important thing priorities you’re taking a look at inside Imagine’s ‘entry to success’ technique?

Primary: We’re going to proceed investing in scaling our artist companies enterprise. Up to now three to 5 years, we’ve created 15 imprints — document labels like KithLabo in Indonesia, PLAYCODE in Japan, and All Night time Lengthy in France. We’re going to proceed doing this.

Precedence quantity two is accelerating, increasing, and deepening our label companies. As a result of the world is extra complicated than it as soon as was, as a result of our labels must reduce by the noise with their artists, the extent of companies they require goes far past easy distribution and financing.

“We need to deepen our partnerships with the DSPs, whether or not it’s Spotify by Discovery Mode, Marquee, or Showcase, or TikTok, or YouTube.”

Now you even have to supply knowledgeable strategic recommendation: What market alerts do you want [in order] to function? What kind of contract? How do you execute advertising?

Precedence three is scaling our publishing enterprise [following the acquisition of Sentric]. We’ve executed quite a lot of work constructing an answer that we expect is now a big aggressive benefit in assortment.

We additionally need to deepen our partnerships with the DSPs, whether or not it’s Spotify by Discovery Mode, Marquee, or Showcase, or TikTok, or YouTube. It’s all about placing these partnerships on the heart of monetizing catalog and creating artists. There’s a significantly better alignment that should occur within the subsequent 10 years with the DSPs.

Our fifth precedence is folks. We have to upskill everybody, in easy methods to do [more sophisticated] digital advertising, to ship higher worth to the artists and labels – and construct the instruments to make that occur. There’s quite a lot of work to do in constructing the software program that our inside groups use to serve their shoppers.

Geographically, the place are you focusing for development?

We’re constructing on our present power in Europe and Asia after which making first-level investments in three particular areas: the US, the UK, and Japan – the world’s largest markets, the place we’ve invested lower than we’ve in different markets [to date].

In Japan, TuneCore Japan is already the third-largest participant when it comes to native market share. We’ve additionally signed a cope with Teichiku and some giant labels to distribution [deals], and we’ve launched the artist companies imprint PLAYCODE round hip-hop.

“We’re making first-level investments in three particular areas: the US, the UK, and Japan.”

Can we break the highest artists in the US and UK tomorrow, as we’ve executed in different territories? Sure, I’ve little doubt about that as a result of we’ve all of the levers [required] on the Spotifys of the world, YouTube, TikTok.

Radio and tv at the moment are much less influential in these markets. It’s only a matter of time.

You’ve stated beforehand that you simply felt there was a definite lack of acquisition alternatives within the UK at scale.

That’s appropriate. Our DNA as an organization is to assist the buildup of native ecosystems, so after I see that within the UK, native artists in 2024 represented simply 28% of streams – that’s a killer for me.

If the UK had the identical price of native artists as you see within the US, Japan, or Brazil at 60-70%, you’d nearly triple the market measurement. Which means extra jobs, extra native labels, extra folks. That provides you greater [domestic] firms, extra affect, and the power to market.

“Once I see that within the UK, native artists in 2024 represented simply 28% of streams – that’s a killer for me.”

Folks say it’s okay that the UK market is small as a result of it exports loads. However guess what – in some unspecified time in the future, in case your home market is just not sturdy, your capacity to export turns into weaker; you might have a tougher time breaking artists regionally.

The UK must escape of that mindset. You should strengthen your native market.

Earlier You talked about Imagine’s use of Spotify Discovery Mode. It’s a platform that’s SPLIT OPINION within the enterprise, however presumably you see it as useful to democratization?

We’ve executed quite a lot of work with Spotify round this. I’m informed that we function Discovery Mode at a bigger scale than anybody else, extra profitably than anybody else.

Over 98% of the tracks we’ve in this system have [provided] considerably optimistic returns; that’s monetary returns, not simply development of streams.

We transfer lots of of hundreds of tracks each month out and in [of Discovery Mode], and that course of is only AI-driven. You need to perceive how the system works to pick out the best tracks – it’s super-technical.

“Over 98% of the tracks we’ve in Discovery Mode have considerably optimistic returns; that’s monetary returns, not simply development of streams.”

It’s a core driver for all of our labels globally. We predict we’re extra environment friendly than anybody at driving digital catalog revenues on Spotify, partially by Discovery Mode.

Discovery Mode’s limitation is just not its capacity to drive revenues and discovery; it really works effectively. It’s its capacity to really assist new artist improvement, hanging the best stability between catalog and frontline artists. That’s the dialogue we’re having with Spotify for the time being.

It seems to me such as you, TCV, and EQT every personal round a 3rd of the brand new, non-public Imagine. How do you stability management, and past capital, what do they convey to the desk?

When it’s essential increase financing capital to make acquisitions in music, you want buyers who’re good.

EQT has executed quite a lot of work round music—they checked out [a potential, pre-IPO] acquisition of Common a number of years in the past and are buyers in Epidemic Sound. TCV has been an investor in [Believe] since 2014 and can also be an investor in Spotify and Netflix. They’re positively good.

The second secret’s strategic alignment. Earlier than taking the corporate non-public, we did quite a lot of work to make sure everybody was aligned on the technique.

“On the general public market, Imagine was considerably undervalued, which prevented us from elevating cash [at the right price] to make giant acquisitions. That’s not a problem.”

The final component is that you really want shareholders who can deploy capital on the proper valuation. On the general public market, Imagine was considerably undervalued, which prevented us from elevating cash [at the right price] to make giant acquisitions.

That’s not a problem.

Your query about stability of energy is fascinating. My view as a founder is it doesn’t matter whether or not you might have 10, 20, or 30 [percent ownership]. These non-public fairness funds make a enterprise out of supporting entrepreneurs and administration groups. So long as you’re aligned on technique and that technique permits you to create worth, you’re in management.

You begin dropping management the day you’re not creating worth.

Are you grateful {that a} sure aggressive takeover try from Warner Music Group final 12 months in the end WENT AWAY?

Sure, we’re blissful. I’m not anti-major; I believe impartial labels could be served very effectively in a serious document label setup. The Orchard and Sony have demonstrated that very effectively.

However once we [mapped out] this new section of development, I informed TCV we don’t need to promote to a strategic purchaser as a result of we expect there’s extra worth to be created right here. So we’re blissful it didn’t occur.

I like Robert [Kyncl]. His crew is wise, and there would have been some strategic worth [from a merger]. But it surely was not what we wished to do.

The place do you assume the subsequent section of distribution and artist companies goes? Listening is changing into extra dispersed and superstardom is changing into more and more uncommon.

I used to be simply wanting on the SNEP figures for H1 2025 in France.

We’re truly main the Prime 200 as the largest document label [by chart market share in France]. However the Prime 200 in France accounted for less than 19.7% of the full market by worth.

In most territories, the [Top 200] accounts for 25-30% of the market, which implies the [biggest] worth is actually within the ‘center’ – outdoors of the highest chart.

“In H1 2025, the Prime 200 [tracks] in France accounted for less than 19.7% of the full market by worth.”

We’re a ‘middle-first’ firm. That’s our DNA – 70% of the [industry] revenues are within the center. We’ve been working in these segments for some time, and we all know how they work. I really feel actually good about our positioning.

However there’s additionally a possibility for us to maneuver up and serve extra artists on the prime. You need to construct a mannequin that gives the best stage of service, with the best offers which are totally different at every stage.

Imagine has not historically served the ‘higher tier’ of artists. Three firms particularly would possibly say you’ll by no means be capable to provide what they provide – have a look at all of the folks they’ve and the cash they will provide upfront. Are these dynamics altering?

I must discover a higher phrase for this, however we thrive with ‘digital artists’. A ‘digital artist’ is only a common artist who creates music, besides the way in which that artist connects, interacts, and will get viewers discovery is digital.

That’s what’s opening up the chance for us [with charting artists] as a result of the market is changing into much less concentrated – it’s much less about radio, it’s much less about tv, it’s extra about partnerships with digital companions, digital advertising.

Due to that, we’re in a position to problem the normal labels on the prime now in a really totally different manner.

What about heading off the risk from the majors within the ‘center tier’, although? They’re reaching into your territory simply as you’re reaching into theirs.

After we take into consideration how we construction offers with Spotify, YouTube, what instruments and companies we develop, we expect ‘middle-first’. That’s very totally different from main document labels – they assume ‘prime’ and ‘international prime’ first.

It signifies that when main document labels function in that [‘middle’] market phase, after they do [artist deals] at a smaller scale, they don’t at all times know easy methods to function with the best economics, with the best financial mannequin vs. the best stage of service.

To some extent that creates confusion available in the market. A variety of time, we see [megastar] artists being served by the groups on the prime with [label services] economics – the economics of the ‘center’, which we all know don’t make sense.

The truth that main labels at the moment are scaling their enterprise [into the middle tier] will pressure them to assume: What economics do I really want to realize right here? How a lot capital do I even need to deploy there versus the [top]?

For us, it’s good as a result of that course of is in the end going to make the market more healthy.

Sony just lately confirmed that it OWNS MINORITY STAKES in round half of The Orchard’s prime 20 shoppers. What do you make of that development?

It’s good and really pure. We do the identical factor!

The labels we’ve seen develop the quickest [at Believe] are the labels the place the high quality of partnership is the best – the place the extent of [collaboration] with the groups round technique, easy methods to develop artists, what market segments to enter, has been the best.

After we can strike these partnerships which are actually shut from a business standpoint after which rework them into minority investments or majority investments, relying on the scenario, we are able to ship most worth and cement these relationships.

The proposed Common/Downtown merger is getting quite a lot of consideration in Europe, with the EC evaluating if it’s anti-competitive in any manner. The place do you stand on it as a contest challenge?

I’ve two solutions.

My first reply when it comes to Europe, together with the UK, is that the primary challenge [for EU/UK lawmakers] might not be the Downtown merger. It’s 28% of streams being from native artists within the UK, 36% in Germany, 41% in France.

What the authorities in Brussels or politicians must be taking a look at is that this: Europe is the largest market from a [music] publishing standpoint. There’s no purpose why it shouldn’t be the most important market from a recorded music standpoint. But it surely’s not.

“Do I believe [UMG buying Downtown] goes to alter something for us? I can’t communicate for the trade, however as CEO of Imagine, we really feel superb about the place we stand and our capacity to compete.”

We should always have politicians targeted very strongly on: What situations do we have to create to enhance [Europe’s] place? How can we foster the event of a powerful native ecosystem? That’s rather more highly effective.

Do I believe [UMG buying Downtown] goes to alter something for us?

I can’t communicate for the trade, however as CEO of Imagine, as an organization, we really feel superb about our capacity to compete.

I believe that we can ship a superior high quality of service to our artists and labels.

To be 100% clear, if you happen to get up tomorrow and Common has totally acquired Downtown, you’re not dropping any sleep?

As I stated, we really feel superb about our capacity to compete.

You talked about market share points with native repertoire. I believed with the rise of impartial hip-hop particularly, native language music was dominating greater than ever in European nations?

That’s the notion, not the fact.

Take a market like France. The primary market phase is local-artist hip-hop. However the quantity two market phase when it comes to revenues and streams? Worldwide pop. Quantity three? Worldwide rock. Quantity 4? Worldwide hip-hop. Quantity 5? French pop.

Now take into account that French pop is one-fifth the scale of the bigger market segments. So [in terms of the total French market] you might have round 60% of the streams which are worldwide music.

“Once more, have a look at the SNEP figures in France: The Prime 200 is 70% native artists. However as quickly as you go beneath the Prime 200 or Prime 500, you go from 70% native to 80% worldwide.”

In Germany, it’s the identical. You might have native hip-hop as the largest market phase, however that’s the one native phase you might have [amongst the most popular genres]. Schlager is just not even within the prime 5.

In contrast, whenever you have a look at China, Japan, Brazil, you see 60-70% of streams from native artists. That’s double the market alternative [for local artists] than we see in European international locations.

It’s tremendous necessary for Europe to rebuild that – it’s straight tied to employment, together with [tax] income and cultural affect.

Once more, have a look at the SNEP figures in France: The Prime 200 is 70% native artists. However as quickly as you go beneath the Prime 200 or Prime 500, you go from 70% native to 80% worldwide.

The highest artists are very effectively supported by the native DSPs throughout all territories. However the backside [sub-Top 200] is being pushed by algorithm-based suggestion, which isn’t as localized accurately. That’s what’s driving quite a lot of the Anglo-American content material.

What could be executed? Name up the EC and say: ‘Neglect UMG/Downtown, nobody cares. Put thresholds on streaming playlists for native artists!’?

I’m not calling for regulation. This isn’t about playlist quotas.

It’s so simple as asking the DSPs to publish, a few instances a 12 months: ‘I’ve delivered XYZ algorithmic suggestions. What number of had been native? What number of had been worldwide? To what market [genres]?’

The DSPs will then be capable to ask themselves questions. I believe they are going to need to develop into good residents of the world [by protecting local artists in their algorithms]. In my expertise, that may be sufficient to affect and transfer the problem by regular business and human incentives.

We’ve seen unspectacular development in streaming subscriptions in H1 2025 in mature markets just like the US, Germany, and France. Do you might have any considerations for the way forward for the enterprise?

With my Imagine hat on, no. We’re positioned in a few of the fastest-growing markets. If we had been extra weighted to the US, UK, or Scandinavia, sure, I might be extra involved as a result of paid streaming adoption is [growing] slower.

There’s loads of development within the present markets for us as an organization, and the truth that a few of these giant markets are ‘new’ territories for us offers us loads of development alternative.

I additionally assume there’s loads of development potential in streaming pricing, each by segmentation, the ‘supremium’ tiers, and basic value will increase.

There’s at all times a dialogue round AI music. Is there hazard coming from Suno/Udio/Anthropic and so forth. or is that this going to be a novelty challenge?

My tackle that is unchanged: marginal income alternative, marginal risk. The entire knowledge I’ve checked out helps this.

Sure, there are increasingly more AI tracks being distributed on the platforms. The most recent knowledge from Deezer exhibits 28% of tracks [being uploaded to the platform] are totally AI. However these tracks are solely producing 0.5% of complete streams.

“You’ll be able to produce as many gen-AI tracks as you need – if there’s not one thing distinctive about them, it’s not going to hit [meaningfully] into the revenues of artists.”

You’ll be able to produce as many gen-AI tracks as you need – if there’s not one thing distinctive about them, it’s not going to hit [meaningfully] into the revenues of artists.

I’m not too involved about it. I believe the entire tech gamers have an curiosity in behaving correctly.

I might be anxious if I believed Spotify or one other service was going to make use of this to decrease their content material prices. But it surely’s nearly inconceivable for them to do this as a result of their enterprise is based on working with artists.

Music Enterprise Worldwide has run quite a few headlines prior to now 12 months about cuts at bigger music firms. Is Imagine transferring in the wrong way?

Sure, we’re investing. In 2024 there have been a number of international locations the place we made changes, however globally, our headcount continued rising. And it’s going to develop once more in 2025.

That’s being pushed by market development. We’ve got alternatives in publishing, so we’re hiring folks on the publishing aspect. And as I stated, we’re constructing new label imprints because the markets develop into extra digital.

“Globally, our headcount continued rising in 2024. And it’s going to develop once more in 2025.”

The most important distinction between us and the foremost document firms is that the Imagine mannequin was created initially as a worldwide mannequin. Our accounting, authorized, monetary groups – all of our tech methods – are already totally built-in and streamlined.

Main labels had been constructed as basically monetary holding firms of native companies, at a time when CD manufacturing logistics had been principally native. They haven’t but executed the transfer of actually streamlining their companies [to be global]. Additionally they haven’t totally addressed: What’s being generated by catalog? What’s the actual profitability of my frontline label? What ought to the stability be?

While you’re rising actually quick, you’ll be able to conceal that. While you develop slower, it’s rather more troublesome.

Common is suing you within the US; the primary allegation is that a considerable amount of uploads through TuneCore have infringed copyright. Do you might have an replace on that scenario?

We don’t touch upon pending litigation. [Believe has previously said it “strongly refutes” UMG’s claims, and “will fight them”.]

If I might provide you with a magic wand to alter one factor in regards to the music trade right this moment, what would you modify?

I’ve been anticipating this query.

The document trade already has the magic wand in its hand. We’re already shaping the way forward for music – we’re shaping it once we’re having conversations with Spotify, YouTube, and others.

We’ve got sufficient affect collectively as an trade to have the ability to ensure that the way in which these applied sciences are being rolled out will likely be in a manner that creates worth.Music Enterprise Worldwide

{kind=link}